நிதி உதவி வழங்க !

UPI ID : enb@axis.com

UPI ID : enb@axis.com

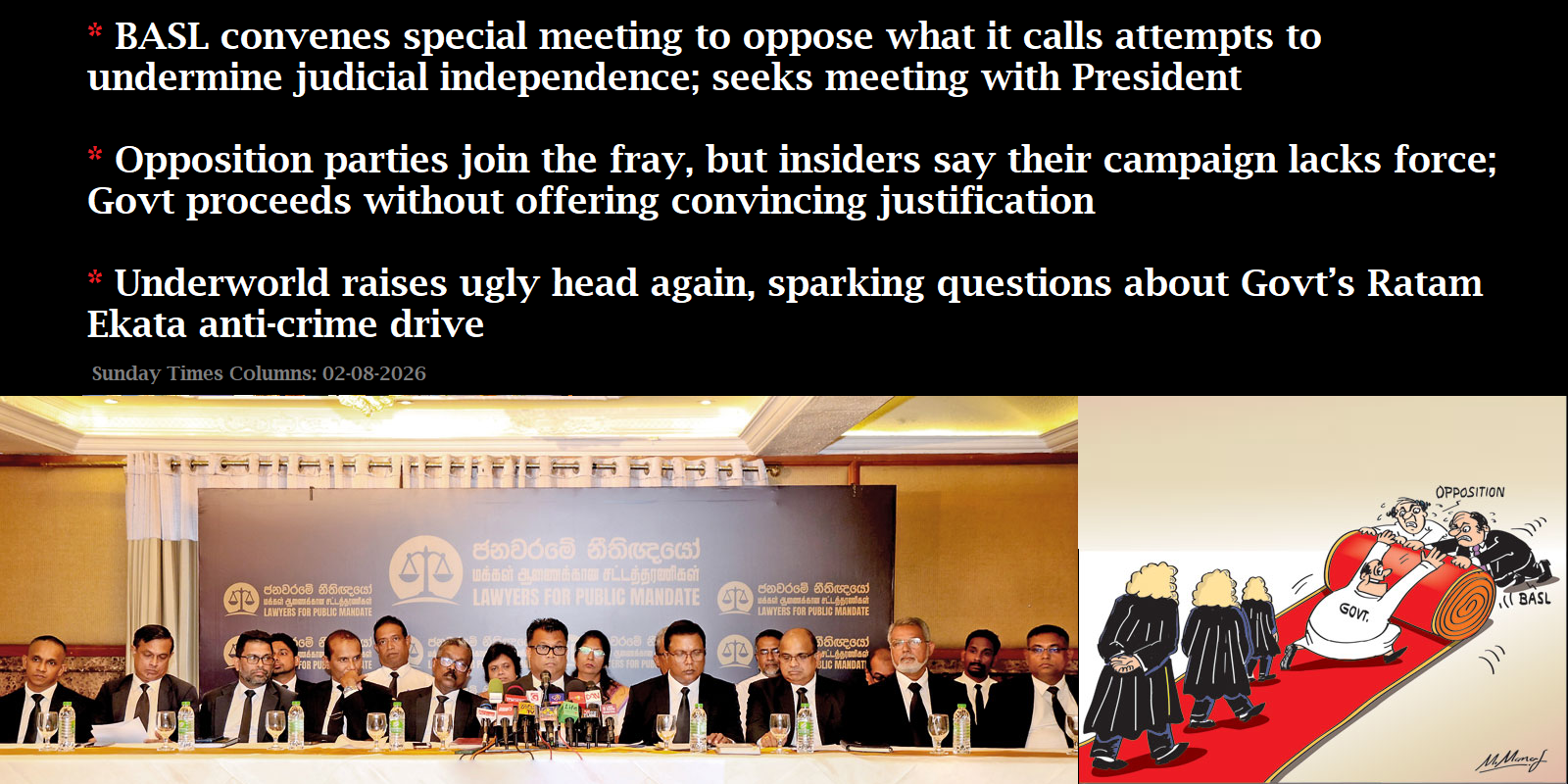

As prison riots add to its woes, Govt resists dropping move to extend judges’ retirement ageDespite NPP’s manifesto pledge to reform prisons, no comprehensive plan in placeCorruption within prison system is as much a concern as overcrowdingOpposition escalates campaign against amendment; legal challenge loomsIndian foreign secretary’s visit sparks renewed calls for provincial council elections By our ST Political Desk 09-08-2026Before taking power, the National People Power (NPP) seemed to have understood the problems embedded in the country’s prison system, going by the contents in its election manifesto ‘A Thriving Nation, a Beautiful Life’. But two years on, instead of any meaningful steps being taken to put the system in order, the situation has worsened inside prisons with uprisings by inmates in several facilities within the past three weeks and fears that there would be more in the weeks ahead.While some government seniors have hinted at a ‘conspiracy’ behind the spate of incidents of unrest in prisons, overcrowding seems to be the main problem leading to the unrest. While overcrowding has been a problem for many years, the situation has worsened in the past two years with the prison population jumping from 29,000 to 40,000, while the NPP’s pledges of a ‘humanitarian prison – a lawful confinement” are long forgotten.This week there was unrest in four prisons – Mahara, Magazine Remand Prison (Colombo), Kuruvita and Pallansena – which left three prisoners dead and scores of others injured. Some of the prisoners died of gunshot injuries after the Police and Social Task Force (STF) personnel were called in to quell the unrest, with the army also deployed outside the prisons for crowd control.Senior DIG Ranmal Kodituwakku, who heads a special rapid deployment unit, was the first to reach the Mahara and Magazine prisons during the unrest, which also led to an attempted jailbreak.“Some of the prisoners had managed to improvise iron rods and other material at hand to try and break the outer walls of the prisons and escape. These were thwarted due to the quick action by the police and STF,” Senior DIG Kodituwakku said. He said tear gas had to be used to bring the situation under control at Mahara and Magazine prisons.Justice Minister Harshana Nanayakkara, under whose purview the Prison Department functions and who survived a no-confidence motion against him less than two weeks ago over the Negombo Prison riots, is once again under fire, including from some within the government. While the NCM was roundly defeated in Parliament, with 152 government MPs voting against it with only 36 voting in favour, some of those who supported Mr Nanayakkara have asked him to rein in the situation in prisons soon or face repercussions.A senior government source who wished to remain anonymous said that at a meeting held on Friday with President Anuara Kumara Dissanayaka to discuss the prison matter, with Public Security Minister Ananda Wijepala, the Justice Minister and Inspector General of Police Priyantha Weerasooriya in attendance, there were some strong words directed at the Justice Minister for the worsening situation in prisons. The President himself had wanted better action plans in place in each of the country’s 32 prisons to avoid any further unrest.On Thursday, Minister Nanayakkara replied to queries raised by MP Dayasiri Jayasekara regarding the prison situation. He acknowledged that prison overcrowding was the main problem. However, without admitting to any fault during his tenure, the minister chose to blame past rulers for the overcrowding issue. “We are facing this crisis because not a single government in the past 20 years has taken any action to develop this infrastructure. This is not a problem that was created after we came to power. But I accept that we must solve it,” he said.A senior official familiar with the government plans, including opening new facilities, releasing remand prisoners on special amnesties and amending the law governing bail for suspects arrested in connection with drug-related offences, said there is no cohesive plan in place to deal with the prison overcrowding except for ad hoc measures that are being announced.“Given that a majority of remand prisoners are those linked to drug-related offences, there are no shortcuts to solve this problem. What has been mooted so far are ‘Band-Aid solutions’ which will not provide any long-term solutions,” he said.The official said that in the NPP’s manifesto, it had been clearly said that the prison had become a place to punish prisoners rather than to reform them, and they have become criminal centres due to drug trafficking and underworld activities – but they remain the same. The main focus where drug addicts are concerned should be rehabilitation, without which releasing them prematurely could lead to a breakdown in the law and order situation. Rushing to release prisoners and changing laws will not help without proper rehabilitation centres and clear-cut programmes such as community programmes,” he said.While the government can formulate programmes to ease overcrowding and provide better facilities, etc., according to sources familiar with the working of the prisons, the recent unrest has been largely due to drug addicts turning violent, unable to get their drug supplies, which they usually did even from behind bars.“It’s an open secret that many of the addicts have access to smuggled drugs inside the prison, but due to the tightening of the security checks, this has become difficult. This is a main reason for their uprisings inside the prisons,” the source said.Corruption within the prison system isn’t helping, with many jailers being accomplices in bending the rules in favour of prisoners, with parallel administrations being run within prisons. “There are separate businesses being run inside the prison by some corrupt jailers. Some charge Rs 1500 for phone charging, Rs 1000 for an extra bucket of water, etc. Unless this kind of insider deal-making is stopped, it’s unlikely the situation in prisons can improve,” he said.With more and more high-profile drug dealers being locked up in recent months, the government’s thinking is that they too may be instigating the unrest within prisons to divert attention from the ongoing crackdown on organised gangs linked to the drug trade.“Due to the recent unrest, hundreds of police, STF and even military personnel have to be deployed to guard prisons. This takes away the resources to carry out raids on criminal gangs, and hence it is possible that they too may be instigating this kind of situation,” a government source said.While corruption within the Prison Department isn’t entirely new, those in the service say it’s a thankless job without proper facilities and safeguards for them.The recent killing of the ten prison officials, having been beaten to death by prisoners, has left their colleagues shaken, and this in turn has led to allegations that prisoners are being subjected to torture and beatings on a regular basis. The situation is worse for prisoners who were transferred from Negombo to other facilities.After the Negombo prison clash, inmates from there were transferred to Welikada, Anuradhapura, Wariyapola, Jaffna, Bogambara, Monaragala, Boossa, Kuruwita, Aguna Kolapalessa, Polonnaruwa, Batticaloa, Kalutara and Pallasena.When asked about the allegations of torture of prisoners, Minister Nanayakkara told Parliament that various complaints have been made on social media sites regarding this matter. He said the ministry secretary has appointed a ministerial-level investigation committee to investigate whether any attacks have been made on the detainees.The Committee for the Protecting Rights of Prisoners (CPRP) has exposed the cruel treatment being meted out to the prisoners and called for proper investigations into such claims.Its members who have been outspoken on the issue claimed that they have received death threats for speaking up on the plight of the prisoners. The CPRP said it has received two death threat letters dated July 17, 2026, and postmarked August 1, 2026, by a group identifying itself as the Patriotic Defence Force and addressed to CPRP executive director Senaka Perera and CPRP convener Sudesh Nandimal Silva.CPRP has lodged a formal police complaint and also notified the Human Rights Commission (HRCSL).Judges’ retirement ageEven as the government grappled with the problem of rising unrest within the country’s prison system, it continued on with its controversial plan to increase the retirement age of superior court judges. On Friday, the bill for the 22nd Amendment to the Constitution, which will raise the retirement age of Supreme Court and Court of Appeal judges, was gazetted. The draft bill includes provisions to raise the retirement age of Supreme Court judges from 65 to 67 years and the retirement age of Court of Appeal judges from 63 to 65 years. The draft bill also proposes that the Chief Justice retire upon reaching 67 years of age or after completing a term of six years from the date of appointment as the chief justice, whichever comes first. Furthermore, the draft amendment proposes to increase the number of judges on the Court of Appeal (including its president) from 20 to 25.Also published in the gazette on Friday was the Judicature (Amendment) Bill, which aims to increase the number of judges on the High Court and increase the retirement age of High Court judges and all other judges. Accordingly, the draft bill includes provisions to increase the number of High Court judges from 110 to 120. It also proposes to raise the retirement age of High Court judges from 61 to 63 years. In addition, the retirement age of all other judges and magistrates has been stipulated at 62 years, notwithstanding the provisions of the Public and Judicial Officers (Retirement) Ordinance.Meanwhile, the government’s moves to amend the Constitution to extend the retirement age of superior court judges continue to draw local and international concern. This week, the International Association of Judges (IAJ), the world’s largest organisation representing national judges’ associations, released a statement stating that it shares the serious concerns expressed by many other entities, including the Judicial Service Association of Sri Lanka and the Commonwealth Lawyers Association, regarding the proposed amendment.“From the perspective of the IAJ, it is (i) the timing of and the manner of introduction of, and (ii) the widely perceived reason for this proposed legislation, that causes us to be very concerned, rather than the concept, generally, of making changes to the mandatory retirement age of judges,” the statement noted.The statement stressed that first, the timing and the manner of introduction of such proposed legislation ought not to be on the basis of an “arbitrary, ad hoc, and peremptory announcement”, as the case here, but that it should rather be on the basis of a “reasoned, principled, consultative, and robust procedure of constitutional amendment”. Otherwise, the independence of the judiciary is threatened, the Association emphasised.Second, where it is perceived by many knowledgeable observers that such proposed legislation is designed to benefit a specific judicial officer, or officers, as here, regardless of whether that was, in fact, the government’s intention or not, the independence of the judiciary is undermined, the statement pointed out.Founded in Salzburg, Austria, in 1953, the IAJ represents 93 national associations of judges from five continents around the globe. The Association’s statement is yet another serious blow to the government’s credibility and is yet more evidence that it has so far failed to allay fears, especially within the legal community, that it is determined to push ahead with the controversial amendment because it wants to keep certain judges on the bench for longer and push others out. If that is indeed the motive, it would certainly amount to a blatant interference with the judiciary, no matter how often and how vociferously the NPP and its backers deny it.As the IAJ statement pointed out, the timing and the manner of introduction of the proposed constitutional amendment, as well as the perceived reason for such an amendment to be submitted at this time, are the issues that have given rise to the significant opposition against the draft legislation. For one, the process of drafting the amendment has been shrouded in secrecy. There was no prior consultation with the various stakeholders, particularly within the legal community, regarding the proposed amendment. This was despite it being known at least since April that the government was mulling changing the Constitution to raise the retirement age of superior court judges.The government’s initial response after its plan was exposed by former Justice Ministers G.L. Peiris and Wijeyadasa Rajapakshe was to simply say that such an amendment had not been discussed by the Cabinet. This position was soon abandoned, however, with a public acknowledgement that the matter had been discussed and an assurance that the views expressed by both those for and against the amendment would be taken into account when taking a decision. There was no indication, though, that the government had actually listened to both sides before deciding to go ahead with the plan. One would do well to remember that Justice and National Integration Minister Harshana Nanayakkara only gave the Bar Association of Sri Lanka (BASL) a meeting to discuss the matter last week after the Association voted overwhelmingly to oppose the government’s proposed constitutional amendment. The BASL had also sought a meeting with President Dissanayake to discuss its concerns over the proposed amendment, but no such meeting had taken place up until yesterday.Critics also note that initially, the government was only interested in raising the retirement age of superior court judges through a constitutional amendment. They charge that the amendment to the Judicature Act to raise the retirement age of lower court judges was only announced in the face of fierce opposition to the proposal to raise the retirement age of Supreme Court and Court of Appeal judges.The government’s justification for raising the judges’ retirement age is that it will keep experienced judges in service longer, aiding efforts to clear a backlog of more than 1.1 million pending court cases. This reasoning, however, has been challenged, with those opposed to the government’s plans pointing out that no effort has been made towards filling existing vacancies in the superior courts. With the retirement of Court of Appeal Judge Dhammika Ganepola in May, there are currently as many as eight vacancies in the superior courts (four each in the Supreme Court and the Court of Appeal). Again, the justification given by those within the government regarding the delay in filling superior court vacancies is that the government wants to fill the vacancies in the lower courts first since this is where most cases are pending.Nevertheless, the fact that eight vacancies in the superior courts have been left unfilled for more than three months has led to accusations that the NPP government is keeping these positions vacant as a form of inducement for lower court judges, some of whom might be pressured into delivering judgements favourable to the government. This may not be the government’s intention, and indeed, senior ministers have bristled at such accusations. They insist that even the suggestion that judges could be persuaded to deliver favourable judgements in hopes of promotion to the superior courts is insulting to the judiciary. The problem for the government, however, is with perception, and as long as the vacancies remain unfilled, there will always be those who will question the prolonged delay.While the BASL has been leading the Bar’s opposition to the proposed constitutional amendment, opposition parties have been campaigning against it on the political front. The United National Party’s (UNP) Working Committee, which met this week, passed a resolution calling on the government to suspend the proposed constitutional amendment for the moment.Clearing the backlog of cases is the expectation of all parties, the party said after the meeting. In this regard, the UNP noted that the Ranil Wickremesinghe government took steps to obtain a “Governance Diagnostic Assessment” in consultation with an International Monetary Fund (IMF) technical team.The party observed that the assessment report’s observations on the backlog of cases specifically point out that the backlog affects the lower courts, with the annual workload of district judges being about 2000 cases, while magistrates handle over 5000 cases per year.Especially in the Commercial High Court, there is a clear lack of sufficient staff to support court administrative work and judicial research, the UNP stated, quoting the report. It usually takes 6-7 years to enforce a contract in Sri Lanka, and severe delays can be seen as the norm. Matters related to the recovery of money are the most common type of case before the High Court.In addition to improving the capacity of Alternative Dispute Resolution (ADR) mechanisms, judicial procedures should be comprehensively reviewed and revised to encourage speedy resolution and minimise trial time, the party statement noted, while stressing that the evaluation report nowhere mentions the need to extend the tenure of judges.Given these facts, the government’s argument for extending the retirement age of judges is in no way acceptable, the party has emphasised. Instead of pushing ahead with the plan to increase the retirement age of judges, Parliament should first discuss the report prepared by the IMF’s technical team. Before that, the views of the Attorney General, Judiciary and the Bar Association of Sri Lanka can also be taken in this regard, and a new methodology can be formulated, the UNP proposed. After suspending the proposed constitutional amendment, the government should discuss a new system to clear the backlog of cases with all relevant parties, prepare it and present it to Parliament. “It should then be proposed by the Ministry of Justice, and we will fully support it,” said the UNP.The main opposition Samagi Jana Balawegaya (SJB), meanwhile, handed over to Speaker Jagath Wickramaratne a resolution calling for the appointment of a Parliamentary Select Committee (PSC) to obtain proposals for accelerating the hearing and resolution of a backlog of approximately 1.1 million cases pending in the judicial system. A group of SJB MPs led by Opposition Leader Sajith Premadasa handed over the resolution to the Speaker on Tuesday (4). The submission of a resolution calling for a PSC to be appointed on the matter followed a decision reached during the recent meeting of opposition parties at the Opposition Leader’s office in Colombo.Both those for and against the proposal to increase the retirement age of superior court judges have also been lobbying influential religious leaders regarding the matter. The Church of Ceylon (the Anglican Church in Sri Lanka) has already come out publicly against the government’s constitutional amendment. Other religious leaders, however, have remained silent.Representatives of the BASL were in Kandy earlier this week to brief the Mahanayake Theras regarding the proposal to raise the retirement age of superior court judges. After his meeting with the Mahanayake Thera of the Malwathu Chapter, BASL President Rajeev Amarasuriya told the media that the Thera informed him that the chief prelates of the Malwathu, Asgiriya and Ramanna Chapters had sent a letter to the President expressing their opposition to the proposed constitutional amendment.Government sources disputed this, with Justice Minister Nanayakkara telling Parliament that he had not received such a letter, nor had the President informed him of receiving such a letter. Minister Nanayakkara and Cabinet Spokesman Nalinda Jayatissa subsequently visited the Mahanayake Theras as well, with Minister Jayatissa claiming that the prelates had accepted the government’s explanation and did not express opposition to the proposed judicial reforms. Ministers Nanayakkara and Jayatissa also called on Colombo’s Archbishop Malcolm Cardinal Ranjith to brief the Catholic Church regarding the proposed judicial and prison reforms. Neither the Mahanayaka Theras nor the Catholic Church has so far commented publicly on the proposed amendment.The government has also been staunchly defending the proposed amendment in Parliament. “Raising the retirement age of judges is merely a very small part of the overall judicial reform process,” Minister Nanayakkara told Parliament on Tuesday in response to a question raised by Mr Premadasa. He added the government has been implementing reforms from the day it assumed office. “We must prevent trials from being delayed and citizens from being dragged through the courts needlessly. The public has realised that, in the past, individuals who committed wrongs were acquitted after changes of government due to cases dragging on indefinitely,” he claimed.Upon coming to power, the government increased the number of courts in Colombo, the minister pointed out. Eleven High Courts with high case backlogs have been identified, and proposals have been made to establish 11 High Courts outside Colombo. The numbers of small claims courts and commercial high courts have been increased, as have trial-at-bar high courts. Steps are being taken to recruit the necessary judges to hear trial-at-bar cases outside Colombo. Arrangements are also being made to temporarily establish Courts of Appeal outside Colombo.The minister said recruitment of new magistrates is currently under way. There is an insufficient number of magistrates, so interviews will have to be called once again. New court buildings are being constructed and supplied with the necessary facilities. Furthermore, to address the acute human resource shortage in the Attorney General’s Department, steps have been taken to recruit new state counsel and grant promotions. Measures have also been taken to recruit officers to the Government Analyst’s Department and provide them with the required resources, Minister Nanayakkara elaborated. “Extending the retirement age of judges while implementing these judicial reforms remains just a minor part of the broader reform work.”With the 22nd amendment now gazetted, opposition parties are preparing legal challenges to the draft bill in the Supreme Court. They will also be continuing their fight against the draft amendment outside Parliament and the courtroom. SJB General Secretary Ranjith Maddumbandara told the Sunday Times that opposition parties will be calling on foreign diplomatic missions in Colombo in the coming days to brief diplomats about the damage the proposed constitutional amendment will cause to the independence of the judiciary. They will also be holding joint public meetings at the district level to educate the people about the harm the amendment will cause, he added.Sri Lanka Podujana Peramuna (SLPP) General Secretary Sagara Kariyawasam agreed, claiming that the government is trying to abuse the power of the judiciary through the proposed constitutional amendment. The power of the executive, coupled with the power of the judiciary, could destroy the country if it became aligned, he warned. He claimed that it has now come to a point where the very survival of the government seems dependent on it passing the amendment. “I believe the government will move ahead with this amendment even if the entire country opposes it. This is because they know it is needed for them to move forward with their agenda and to crack down on all those who oppose it,” said the SLPP general secretary.Speaking on grounds of anonymity, a senior government source heaped scorn on allegations the government’s proposed constitutional amendment amounted to an interference with the judiciary. He pointed out that the NPP government has been in power now for 22 months. The present Attorney General was appointed under the previous government but has continued to serve under the current administration, he pointed out. “We also appointed the senior-most justice on the Supreme Court as the CJ. We didn’t parachute people in from outside and made them CJ, unlike some previous presidents,” he quipped. He claimed there is currently a “misconception” that the government is trying to interfere with the judiciary by giving a two-year service extension to the present CJ but insisted one cannot control the judiciary in such a way.He pointed to ongoing delays in court cases involving politicians and other politically aligned individuals. Sometimes, this is due to delays at the Attorney General’s Department or other agencies. There are also delays owing to writ petitions and fundamental rights petitions being filed in the superior courts. The courts have already granted certain orders that have prevented investigations from proceeding further in relation to certain individuals, said the source. “If the courts are subservient to us, such delays would not occur. The government did not control the courts before this amendment, and neither will it control the courts afterwards. The judiciary is independent.”Court cases are now being filed against many politicians, he pointed out. “If they go to prison, even if they get out, their chances of successfully re-entering politics are low. This is why they are so afraid of these court cases. They also know that this is not the type of President who will grant pardons to convicted politicians, unlike those who occupied the position previously,” the source remarked. He said the government expects opposition parties to go all out against the constitutional amendment in the coming days but insisted the government will be equal to the task.Indian foreign secretary’s visitIndo-Lanka relations were in focus this week when India’s Foreign Secretary Vikram Misri visited Sri Lanka. There’s always been hide-and-seek in the India-Sri Lanka relations, with the two sides rarely speaking in one unified voice in matters of mutual interest, but these usually get buried under the layers of diplomatic jargon that come out in statements after high-level engagements.However, after Mr Misri’s latest trip to Colombo, where he met with President Anura Kumara Dissanayake, some of the contents contained in the press releases issued by the Indian Ministry of External Affairs were missing from the statement issued by the President’s office in Colombo.This was with regard to the holding of the long-delayed elections to provincial councils as well as the full implementation of the Thirteenth Amendment to the Constitution. The statement by the Indian MEA said the visiting Foreign Secretary also “called upon the Sri Lankan leadership to implement their commitment to hold Provincial Council elections at the earliest and to fully implement the constitutional provisions of Sri Lanka to meet the aspirations of the Tamil people.”However the President Office was mum on this matter and instead chose to focus on progress of Indian projects in the country, humanitarian assistance, regional challenges of drug trafficking, climate change, etc.SJB MP Nizam Kariappar, who is in the Political Council of the Tamil-Speaking People, was among those who welcomed Mr Misri bringing up the issue of PC polls with the President. “The Political Council of Tamil Speaking People notes with gratitude that the Indian Foreign Secretary has, as promised, taken up the issues we raised with the High Commissioner. As promised, the High Commissioner briefed the Foreign Secretary immediately, on the eve of his arrival in Sri Lanka. We appreciate this prompt and constructive engagement,” Mr Kariapper said on his X handle.The group had met with Indian High Commissioner Santosh Jha hours before the Indian Foreign Secretary arrived in Colombo. During the meeting, the delegation discussed its ongoing efforts to secure the long-overdue Provincial Council elections and expressed the hope that the Government of India would continue to support these efforts while noting that India had played a pivotal role in the establishment of the Provincial Council system in Sri Lanka through the Indo-Sri Lanka Accord.

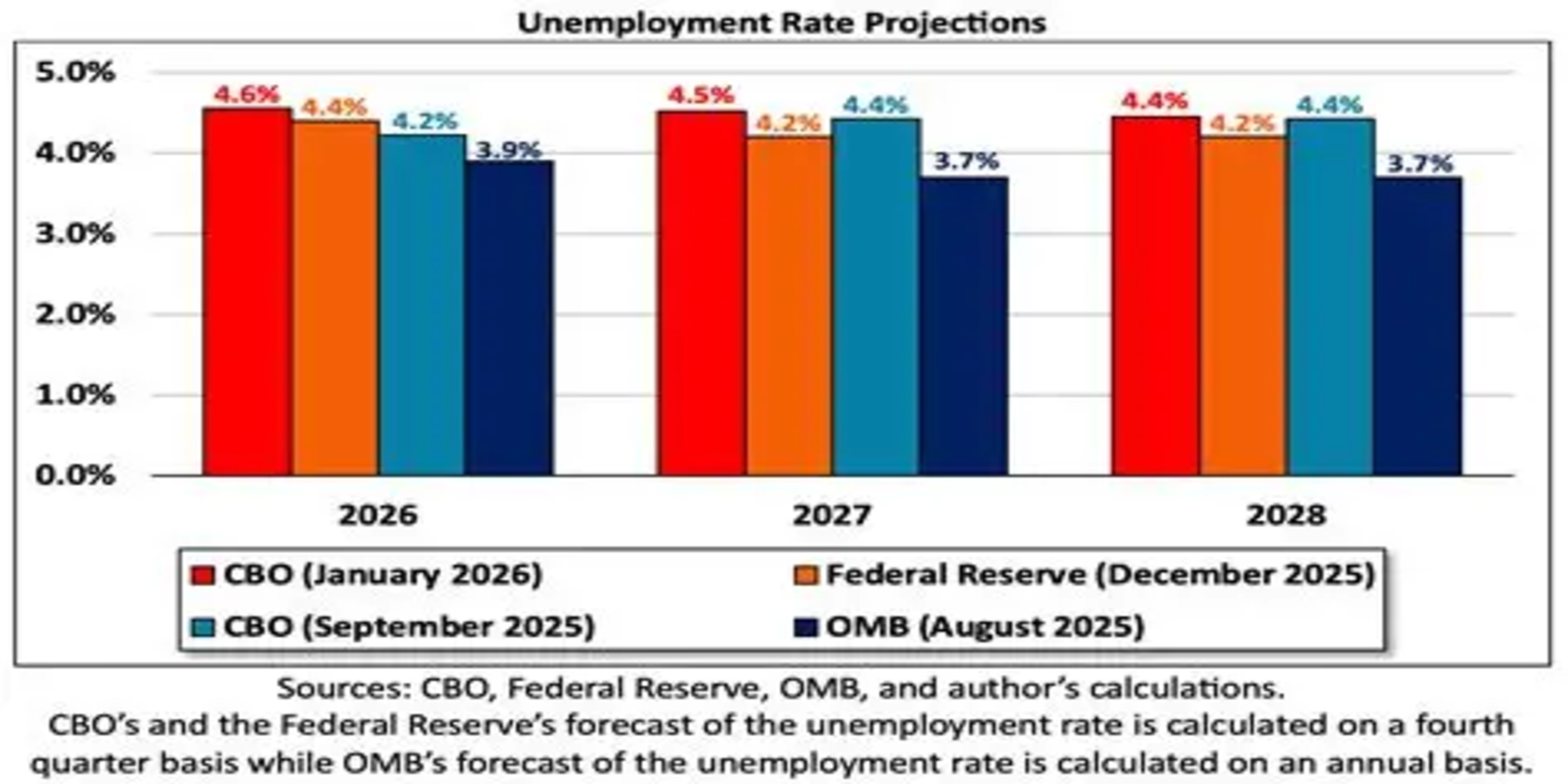

Unemployment improved, because thousands of workers disappeared. Where did they go?The percentage of American workers ages 25 to 54 declined this year, and that’s not a good sign for the economy, experts say.August 8, 2026 By Steve Thompson and Lauren Kaori GurleyThe U.S. economy shed jobs in July, yet the unemployment rate improved — an unusual pairing that points to a worrying story unfolding behind the numbers for some economists.That’s because even as the U.S. economy lost jobs, American workers left the labor market faster.Get a curated selection of 10 of our best stories in your inbox every weekend.“This is one of the very, very few times where you see the number of jobs shrink but the unemployment rate falls,” said Stephen Moore, a conservative economist. The explanation, he said, is fewer people looking for jobs. “That’s a big economic story: Where are the workers?”The share of adults working or looking for work slipped to 61.4 percent in July, extending a weakening in the labor force participation rate this year. That rate has reached the lowest level since February 2021, during the pandemic.Employers shed 23,000 jobs in July, according to Labor Department figures released Friday, and the unemployment rate fell slightly to 4.1 percent from 4.2 percent, due in large part to fewer workers in the labor market.The aging population is one of the bigger forces leading to fewer workers. As baby boomers retire, they pull down the share of adults either working or looking for work. But that doesn’t explain the full drop this year in the labor force participation rate.The share of workers in their so-called prime working years, ages 25 to 54, fell sharply between May and June, and only partially recovered in July, leaving economists to fear that young and middle-aged people are abandoning job searches.Men in particular have been seeing a sharp decline in the workforce, with participation at an all-time low outside of the peak of the pandemic, at 66.8 percent in July, with both older men and the youngest men in the workforce driving the decline. That’s concerning for both social and economic reasons, Moore said. “That is not a good trend.”“We’re just not seeing males working as much, and I don’t have a good explanation for why that is,” he said.A shifting economy plays one role. Most recent job growth has come in health care and private education, fields long dominated by women. Several male-dominated industries, including manufacturing, transportation and mining, have shed jobs over the past year. That leaves a mismatch between the skills many men have and the jobs available.The decline is a potential warning sign, many economists say.“We like to see the unemployment rate go down typically, right?” said Alexander Bick, an economist at the Federal Reserve Bank of St. Louis. But that’s because it normally indicates employment is going up.Bick has watched the labor force participation rate fall for months, and he says it’s “a worrying trend.” The fear is that discouraged workers are giving up.But the picture is not yet clear, because other factors are also playing a role, including the Trump administration’s big push to seal borders, stop immigration and deport immigrants, which has led to a decline in foreign-born workers.Teens and young adults have also fallen out of the workforce. The share of 16- to 19-year-olds working or looking for work has fallen this year, hovering near the lowest levels since the pandemic after teen employment surged in 2023 and 2024. The share of 20- to 24-year-olds in the workforce has also fallen in recent months.One reason some teens are not working is because more are graduating high school, reflected in rising high school graduation rates, experts say. But another reason is weaker hiring in the hospitality and retail sectors, which tend to employ young people.Growth in artificial intelligence and other technologies may also be creating new barriers to entry-level roles. For example, self-service kiosks have taken the roles of many cashiers, said Sara Estep, an economist at the Center for American Progress, a liberal think tank in Washington. Also, A.I. applicant screening tools could be favoring more experienced workers.Estep said she worries that young people are missing out on work experiences that could help them gain a foothold in the labor market for years to come.There is one bright spot from the latest jobs report, said Guy Berger, director of economic research at the Burning Glass Institute, a Philadelphia think tank that studies the labor market. Even as workers have left the workforce, the number of people who say they want a job but have given up searching over the past month has ticked slightly down.“The things that would make me really worried about labor force exits aren’t showing up,” Berger said. “People aren’t telling us, ‘I want a job but can’t find one.’”

தேசிய சுய நிர்ணய உரிமைக் கோட்பாட்டை பேரப் பொருளாக்கும் அரசியல் போக்குக்கு முற்றுப்புள்ளி இடுவோம்!23-07-2026, கறுப்பு ஜூலைப் படுகொலையின் 43 ஆம் ஆண்டு நினைவு-நிறைவு தினமாகும். இப்படுகொலை நிகழ்வு ஈழவிடுதலைப் புரட்சியில் ஒரு முக்கிய திருப்புமுனையும் புதிய பரிமாணமும் ஆகும்.ஈழப்புரட்சியின் ஆயுதப் போராட்டம் உள் நாட்டு யுத்தமாகிய திருப்பு முனையும், இந்தியத் தலையீடு மூலம் பிராந்திய-சர்வதேசிய- தன்மை பெற்ற பரிமாணமும் இப் படுகொலையை ஒட்டியே உருவாகின.உலக,பிராந்திய, உள்நாட்டு சூழல்கள் இன்று பெரிதும் மாறிவிட்டன.இன்றைய சூழலில் ஈழப் புரட்சியை தொடர கடந்து வந்த, குருதி வடித்த காலத்தின் படிப்பினைகள் இன்றியமையாதவை.சுமார் நான்கு தசாப்தங்களுக்கு முன்னால்;1) உலக நாடுகள் அமெரிக்க முகாம், ரசிய முகாம் என இரு முகாம்களாக பிரிந்து இருந்தன. அணிசேராமை என்பது கூட ஏதோ ஒரு அளவில் பின் கதவால் அணி சேர்ந்துதான் இருந்தது.2) இந்தியா அரசியல் ரீதியாக வெளிவிவகாரங்களில் ரசியாவைச் சார்ந்தும், பொருளாதார ரீதியாக பிரித்தானியா மற்றும் அமெரிக்காவைச் சார்ந்தும் இருந்தது. எனினும் பொதுவான ஏகாதிபத்திய நலன் சார்ந்த பிரச்சனைகளில் குறிப்பாக தொடர் காலனியப் பிரச்சனையில் கூட்டாக ஏகாதிபத்தியவாதிகளுக்கு சேவகம் செய்துவந்தது.இந்து சமுத்திரப் பிராந்தியத்தில் ஏகாதிபத்தியவாதிகளின் காவல் நாயாகவும், தலைமைத் தளபதியாகவும் விளங்கியது.3) இதன்காரணமாக தேசிய ஒடுக்குமுறையின் மீது கட்டப்பட்ட தொடர்காலனிய இலங்கை அரசைப் பாதுகாப்பது அதன் பொறுப்பும் கடமையுமாக இருந்தது. ( இந்திய இலங்கை ஒப்பந்தம் இதை சட்டபூர்வமாக்கியுள்ளது)4) மேலும் இந்திய ஆளும் வர்க்கம் தரகுப் பெருமுதலாளித்துவ, பெரு நிலப்பிரபுத்துவ பிற்போக்கு வர்க்கமாகும். இதனால் அது தன் சொந்த நலன் என்ற வகையிலும் அகண்ட பாரத விரிவாதிக்க திட்டம் கொண்டது.5) எனவே இலங்கையில் ஒரு தேசிய ஜனநாயகப் புரட்சி-(1983 இல் இது ஆயுதமேந்திய ஈழப்பிரிவினை-உள்நாட்டு-ப் போராக வெடித்தது) இந்திய ஆளும் வர்க்கத்தின் நலன்களுக்கு அடிப்படையில் முரணானது. அதாவது கட்சி பேதமின்றி, இந்திய அரசின் வர்க்க நலனுக்கும் ஈழதேசிய விடுதலைப் புரட்சிக்கும் இடையிலான முரண்பாடு பகைமையானதாகும். இந்திய அரசு ஈழதேசிய விடுதலைப் புரட்சியின் எதிரி ஆகும். 6) எண்பதுகளில் இலங்கையில் ஒரு கட்சி என்கிற வகையில் ஐக்கிய தேசியக் கட்சி ( United National Party-UNP) - முழுமையாக அமெரிக்க மேலை ஏகாதிபத்திய, வர்த்தகத் துறையில் ஜப்பானிய ஏகாதிபத்தியத்தைச் சார்ந்து முந்நிலையில் இருந்தது.7) 83 ஜூலைப் படுகொலை பெருமளவிலான தமிழ் மக்களை பாக்கு நீரிணைக்கு அப்பால் தூக்கி வீசியபோது, ஜப்பானியச் சந்தையைக் கைப்பற்றுவதற்கான அரிய வாய்ப்பை இந்தியா கண்டது.இந்திரா கடித்த இந்த அப்பிள் பழத்துடன் தான், தமிழர்களுக்கு எதிரான இந்திய அரசின் `ஆதிப்பாவம்` ஆரம்பமானது!8) இதற்குத் துணை போன தமிழக மாநிலத் தரகர்கள் இதை ``தொப்புள் கொடி உறவு `` என்றனர்!9) இந்தத் தகாத உறவில் குறைமாதப் பயிற்சி முகாம்களில் இருந்து நூற்றுக்கணக்கான குயில் குஞ்சுகள் ஆயுதங்களோடு பொரித்து இலங்கைக்குள் நுழைந்தன.10) இவ்வாறு `எல்லை தாண்டிய பயங்கரவாதம்`, ஜே.ஆர் அரசைப் பணியவைக்கும் பயங்கரவாத நடவடிக்கைகளில், றோ அமைப்பால் வழி நடத்தப்பட்டது.அப்பாவிச் சிங்கள மக்கள் மீது இராணுவ வன்முறை கட்டவிழ்க்கப்பட்டது.எல்லைப் புறத்தில் தமிழர் காணிகளில் பலவந்தமாக குடியேற்றப்பட்ட ஏழை எளிய வறிய சிங்கள விவசாயிகள் வெட்டிச் சரிக்கப்பட்டனர்.இவ்வாறு தான் ஜே.ஆர் அரசு பேச்சுவார்த்தைக்குப் பணிய வைக்கப்பட்டது.11) 1983 ஜூலைப் படுகொலையை ஒட்டி `இந்தியாவைப் பயன்படுத்தி`, பங்களாதேஸ் போல ஒரு தமீழீழ தேசைப் படைக்கக் கிளம்பிய போராட்டக்காரர்களுக்கு, அவர்களது எண்ணத்துக்கு மாறாக தாம் இந்தியாவால் பயன்படுத்தப் படுகின்றோம் என்ற எண்ணம் ஒரு அரசியல் மதிப்பீடாக உருவாகவில்லை.12) இவ்வாறு இந்தியா தலையிட்டபோதும், அதற்கு இனமானம் பேசிய தமிழக தரகர்கள் துணைபோன போதும், அவர்களது உதவியைப் பெற்றபோதும் அந்த உறவை ஒரு கோட்பாட்டு - ஒடுக்கப்படும் ஈழ தேசத்தின் பிரிவினைக்கான ஆயுதப் போராட்டத்தை அங்கீகரி- அடிப்படையில் அமைத்துக் கொள்ளவில்லை.வந்தவரை இலாபம் அல்லது அவர்களைப் ``பயன்படுத்துவது`` என்கிற வகையில் தன்னியல்புச் சந்தர்ப்பவாத வழியைக் கடைப்பிடித்தனர். கட்சிகளுக்கு ஏற்ற வகையில் சுய நிர்ணய உரிமைக் கோட்பாட்டை மாற்றி வளைத்து திரித்து பேசி வந்தனர்.இவ்வாறு சுய நிர்ணய உரிமைக் கோட்பாட்டை ஒரு பேரப் பொருளாகக் கையாண்டனர்.13) இதனால் 1985 திம்புப் பேச்சுவார்த்தையில் இந்தியாவின் நிர்ப்பந்தங்களுக்கு பணிய நேரிட்டது.புலிகள் தவிர ஏனையோர் ஆக இரண்டு ஆண்டுகள் `போராடிக் களைத்து` இந்தியக் கைக் கூலி ஐந்தாம் படை ஆகினர்.இதற்கு முதற் காரணம் குட்டி முதலாளித்துவ வர்க்க இயல்பாகும். இரண்டாம் காரணம் இவ் அமைப்புகள் தனிநாட்டுக் கோரிக்கையை சமஸ்டிக் கட்சியிடமிருந்து அப்படியே கைமாற்றியதாகும்.மூன்றாம் காரணம் EPRLF போன்ற இடது சாரியம் சோசலிசம் பேசிய கட்சிகள், இந்திய திருத்தல்வாத கொம்யூனிஸ்ட்டுக்களிடம் அரசியல் போதனை பெற்றதாகும். Samaran கற்க: மா.லெ.தீர்மானம் (1983-டிசம்பர்) 1976 வட்டுக்கோட்டைத் தீர்மானம்:1976 மே 14 ம் திகதி வட்டுக் கோட்டைத் தீர்மானம்சமஸ்டிக் கட்சியின் தலைமை அருணாசலம்,இராமநாதன், போன்ற நிலப்பிரபுக்கள் வழி வந்த தரகு வர்க்கக் கட்சியாகும்.ஏகாதிபத்திய சார்பு கட்சியாகும். இதனால் தேசியப் புரட்சிக்கு எதிரானதும், இந்திய விரிவாதிக்கத்துக்கு சார்பானதுமான கட்சியாகும்.1977 இல் வட்டுக்கோட்டைத் தீர்மானம் நிறைவேற்றி, பொது ஜன வாக்கெடுப்பில் ஆதரவான மக்கள் தீர்ப்பைப் பெற்ற கட்சி, 1981 இல் மாவட்ட அபிவிருத்தி சபையை இடைக்கால உடனடித் தீர்வு என்று கூறி ஏற்றுக் கொண்டது.1983 ஜுலைப் படுகொலை நடந்த போது தமிழ் நாட்டில் இந்திய அரசின் துணையில் தஞ்சம் புகுந்தது.1985 இல் திம்புக் கோரிக்கைக்குத் துரோகம் இழைத்து இந்தியாவுடன் இணைந்தது.1987 இல் மாகாணசபையுடனும் சட்டபூர்வ துப்பாக்கிகளுடனும் கால் பதித்தது.1947 இல் சமஸ்டி (டட்லி செல்வா-பண்டா செல்வா ஒப்பந்தங்கள் சமஸ்டி அடிப்படையிலான சமரசங்களே-இந்த சமரசத் திட்டத்தின் அடிப்படையில்தான் சமஸ்டிக் கட்சி தமிழ் பேசும் மக்களிடையே ஐம்பது-அறுபதுகளில்,காந்திய வழியில் ஒரு சமூக இயக்கமாக மாறியது), 1977 இல் தமிழீழம், 1981 இல் மாவட்ட அபிவிருத்தி சபை,1985 இல் திம்பு கோரிக்கைக்கு துரோகம், 1987 இல் மாகாணசபை (13ம் திருத்தம்)..... 2009 இற்குப் பின்னால் ஏக்க ரட்டே மந்திர சபை.குறுகத் தறித்த சமஸ்டி இயக்கத்தின் இந்த 80 ஆண்டு வரலாற்றில், `தமிழீழம்` விதி விலக்காக இடைச் சொருகலாக இணைந்திருப்பதை காணுவது கடினமல்ல.உண்மையில் அவ்வாறுதான் நடந்தது.சமஸ்டி என்கிற அரசியல் கோரிக்கை சமரசவாதம் என்கிற அரசியல் போக்காகும். சமஸ்டிக் கட்சியின் வர்க்க அடித்தளம் தரகு முதலாளித்துவ நிலப்பிரபுத்துவ கூறுகளாக இருந்தாலும், அதனுடைய சமரசவாதம் அனைத்து சமூக வர்க்கங்களிடையேயும் உள்ள சமரசவாதக் கூறுகளை அணிதிரட்ட உதவியது. இவ்வாறுதான் சமஸ்டிக் கட்சி தமிழ் பேசும் மக்களிடையே ஒரு சமூக இயக்கமாக மாறியது.ஆனால் புறவய நிலைமைகள் இதை அனுமதிக்கவில்லை. சமஸ்டிக் கட்சியின் சமரசவாதம் வரலாற்றுச் சக்கரத்தைப் பின் நோக்கி இழுக்கும் திசையில் பயணித்தது.சமரசவாதம் எதிர் நீச்சல் அடித்தது.70 களில் ஏற்பட்ட உலக ஏகாதிபத்திய பொது நெருக்கடியின் காரணமாக தொடர் காலனிய இலங்கை அரசின் மீது இடி இறங்கியது.தேசியப் பகைமையை தூண்டி வளர்ப்பதன் மூலம் தனது அரசுமுறையைப் பாதுகாக்க சிங்கள ஆளும் வர்க்கங்கள் ஒன்று மாறி ஒன்று முயன்றன.1972 அரசியல் யாப்பு, கல்வித் தரப்படுத்தல், சோனகர்களுக்கு எதிரான தாக்குதல், திட்டமிட்ட குடியேற்றம், தமிழாராய்ச்சி மாநாட்டுப் படுகொலை, தமிழ் இளைஞர்களின் கைது, சிறை, சித்திரவதை கூடவே சமஸ்டிக் கட்சியின் சட்ட மறுப்புப் போராட்டம் என்பன இக்காலத்தின் குறிப்பிடத்தக்க நிகழ்வுகளாகும்.சட்டமறுப்புப் போராட்டத்தோடு சமஸ்டிக் கட்சி வரலாற்றின் கைதி ஆனது.கற்க: ஈழத்தில் வர்க்கப் போராட்டம் விற்பனையில்-பனுவல் On Line Book Sellersஇந்த இயக்கத்தில் 1978 பொதுத்தேர்தலில் முன்னின்று உழைத்த இளைஞர்களில் ஒரு பிரிவினரிடமிருந்து புதிய பாதை, புதிய தலைமை பற்றிய சிந்தனையும் கேள்விகளும் எழுந்தன.இக்காலப் பகுதியில்தான் பாலஸ்தீன விடுதலை இயக்கம், அயர்லாந்து விடுதலை இயக்கம், விடுதலை, பிரிவினை, வட அயர்லாந்து, பங்களாதேஸ், ஈழம் (தமிழீழம்) என்கிற பொறிகள் தெறித்தன.எனினும் இவை முளைக்க முன்னமே கருக்கப்பட்டுவிட்டன.மிக முக்கியமாக இது சமஸ்டிக் கட்சியைச் சாராமல் அதன் பலத்த எதிர்ப்பைச் சந்தித்து, அதற்கு சவாலாக உருவாகி வளர்ந்து வந்தது.ஈழ விடுதலை இயக்கம் இப்போது தான் தோன்றியது.இவ்வாறு இனியும் தவிர்க்க இயலாத, தணிக்க இயலாத நிலை தோன்றிய போதுதான் சமஸ்டிக் கட்சி தமிழீழத் தீர்மானம் நிறைவேற்றியது. இது 1977 பொதுத் தேர்தலில் வெகுஜன வாக்கெடுப்புக்கு விடப்பட்டு அதிகப் பெரும்பான்மை வாக்குகளால் ஈழ தேச மக்களிடையே வெற்றிபெற்றது.இந்தக் காரணத்தால் வெகு ஜன வாக்கெடுப்பில் தீர்மானிக்கப்பட்ட ஒரு தேசத்தின் முடிவை, அதே மக்களிடையேயான இன்னொரு வெகு ஜன வாக்கெடுப்பின் மூலம் அல்லாமல் அதை மாற்றமுடியாது.அதுவரைக்கும் ஈழ தேசியப் பிரச்சனைக்கு தமிழீழமே தீர்வு.எங்களை ``என்ன பெயர் வைத்து நீங்கள் அழைத்தாலும்`` வேறெதுவும் தீர்வல்ல.நிற்க.இந்த வாக்கெடுப்பு முடிவை _ தேசத் தீர்ப்பை_ ஏற்பது என்பது ஒன்று. பிரிவினைக்காக முன் வைக்கப்பட்ட விளக்கங்களை, வியாக்கியானங்களை ஏற்பது என்பது வேறொன்று.வட்டுக்கோட்டைத் தீர்மானத்தில் தமிழீழப் பிரிவினைக் கோரிக்கைக்கு முன் வைக்கப்பட்ட தர்க்கங்கள் ஜனநாயகப் பண்பு கொண்டவை அல்ல. அவை ஆண்டபரம்பரை, இனத்துவப் பெருமை அடிப்படையில் அமைந்தவை. இதனால் பிரிவினைக்கான புறவய அவசியம் இல்லாது போனால் ஜனநாயக ரீதியாக இரண்டு தேசங்கள் ஐக்கியப் படவேண்டியதற்கான அவசியமோ நிபந்தனையோ வட்டுக்கோட்டைத் தீர்மானத்தில் இல்லை.மேலும் உப கண்டத்தில் ஜனநாயகப் புரட்சிகள் வெற்றி பெறுவதைப் பொறுத்து ஜனநாயகக் கூட்டாட்சியில் இணைவது குறித்த நிலைப்பாடும் இல்லை. (அற்ப தரகு முதலாளிய, குட்டி முதலாளிய வர்க்க சிந்தனையில் சர்வதேசியத்தை எதிர்பார்ப்பது குற்றம் தான்!)வட்டுக்கோட்டைத் தீர்மானத்தின் முதற் பந்தி-பிரகடனம்-கூறுவதாவது:▶ 1976 மே 14ஆந் தேதியன்று (வட்டுக்கோட்டைத் தொகுதியிலுள்ள) பண்ணாகத்தில் கூடுகின்ற தமிழர் ஐக்கிய விடுதலை முன்னணியின் முதலாவது தேசிய மாநாடு, இலங்கைத் தமிழர்கள் தங்களின் தொன்மைவாய்ந்த மொழியினாலும் மதங்களினாலும் வேறான கலாசாரம், பாரம்பரியம் ஆகியவற்றினாலும் ஐரோப்பிய படையெடுப்பாளர்களின் ஆயுதப்பலத்தினால் அவர்கள் வெற்றி கொள்ளப்படும் வரை பல நூற்றாண்டுகளாக ஒரு குறிப்பிட்ட பிரதேசத்தில் தனிவேறான அரசாகச் சுதந்திரமாக இயங்கிய வரலாற்றின் காரணமாகவும் எல்லாவற்றுக்கும் மேலாக தமது சொந்தப் பிரதேசத்தில் தம்மைத்தாமே ஆண்டுகொண்டு தனித்துவமாகத் தொடர்ந்திருக்கும் விருப்பம் காரணமாகவும் சிங்களவர்களிலிருந்து வேறுபட்ட தனித் தேசிய இனமாகவுள்ளனரென, இத்தால் பிரகடனப்படுத்துகின்றது.ஒரு தேசத்துக்கான-`` தேசிய இனம்``- வட்டுக்கோட்டைத் திர்மானத்தின் வரையறுப்பு விஞ்ஞானக் கேடான அபத்தமாகும். இதில் மிகவும் முக்கியமானது, '` எல்லாவற்றுக்கும் மேலாக தமது சொந்தப் பிரதேசத்தில் தம்மைத்தாமே ஆண்டுகொண்டு தனித்துவமாகத் தொடர்ந்திருக்கும் விருப்பம்`` ஆகும்!இனி, மேலே விட்ட இடத்துக்கு வருவோம்... ' இதற்குக் காரணம் இவர்கள் தனிநாட்டுக் கோரிக்கையை சமஸ்டிக் கட்சியிடமிருந்து கைமாற்றியதாகும்`, என்று மேலே கூறினோமே அது இது தான்.இங்கேதான் சமரசத்துக்கான சந்தர்ப்பமும், சந்தர்ப்பவாதமும் உள்ளது.தமிழீழம் ஆண்டபரம்பரைக்கான, அதாவது தமிழ் பேசும் தமிழருக்கு மட்டுமான, தனித்துவமான நாடு-அல்லது நிலப்பரப்பு- என்றால் 1) அது நித்தியமானது, நிரந்தரமானது, மாறாதது, `` தொடர்ந்திருக்கும்'`!2) அதை ஆளும் உரிமை -இறைமை-தமிழ் பேசும் தமிழருக்கு மட்டுமானது, அதாவது அதன் ஆளும் வர்க்கங்களுக்கானது.3) தமிழீழம் ஒன்றே தீர்வு, அதற்கே சண்டை என்றால் அது இல்லாத அல்லது இயலாத சூழ் நிலையில் சரணாகதி தீர்வாகிவிடும்.ஏனெனில் சுயநிர்ணய உரிமை என்கிற ஜனநாயக நிலைப்பாடு இல்லாமல், இறைமை என்கிற ஆளும் வர்க்க நிலைப்பாட்டைக் கொண்டிருந்தால், ஆளுவதற்கு தமிழீழம் இல்லையென்றால் இப்போதைக்கு அதைவிடக் குறைந்த, ஆளுவதற்கு முழு அதிகாரம் இல்லையென்றால் இப்போதைக்கு அதைவிடக் குறைந்த அதிகாரம் கொண்ட மாவட்ட சபையை, மாகாண சபையை, இடைக்கால அதிகார சபையை ஆள நினைப்பதில் என்ன குறை? தமிழனைத் தமிழன் தானே ஆளுகின்றான்!4) இதைவிடக் கொடுமை என்னவென்றால் இந்த இனத்துவ தமிழீழ-தேசிய-த்துக்கு அந்தத் தேசத்தின் இதர மக்கள் சமூகங்களை அரவணைக்க, அணிதிரட்ட வேண்டிய அவசியம், திட்டம் தேவைப்படாது.திம்புப் பேச்சுவார்த்தை: திம்புப் பிரகடனம் 1985 ஜூன்-ஜூலையில் பூட்டான் நாட்டின் தலைநகர் திம்புவில் திரை மறைவாக நடைபெற்றது. ஆயுதக் குழுக்களும், நாடாளமன்ற சமஸ்டிக் கட்சியும் ஈழ மக்கள் சார்பில் கலந்து கொண்டனர்.பேச்சுவார்த்தையில் இலங்கை அரசு முன்வைத்தை தீர்மானத்தை அடியோடு நிராகரித்த பிரதிநிதிகள், தொடர்ந்து பேசுவதற்கான விருப்பத்தையும், அத்தைகய ஒரு தொடர் பேச்சுக்கு அடிப்படையாக அமைய வேண்டிய கோட்பாடுகளையும் இரத்தினச் சுருக்கமாக பேச்சுவார்த்தை முடிவில் வெளியிட்டனர்.இதுவே திம்புப் பிரகடனம் என அறியப்படுவது. ஒப்பீட்டில் ஈழ தேசியப் பிரச்சனையை அரசியல் ரீதியில் விஞ்ஞான முறையில் வரையறை செய்த ஒரே அறிக்கை இதுவே ஆகும். இதனால் தான் வட்டுக்கோட்டைத் தீர்மானம்-இறைமை-பேசப்படுகின்ற அளவுக்கு, திம்புக் கோரிக்கை-சுய நிர்ணய உரிமை- பேசப்படுவதில்லை!மேலும் 1985 இல் இலங்கை அரசுக்கு இந்தக் கோரிக்கைகளை வைத்தவர்கள், 1987 இல் இதை இந்தியாவுக்கு வைக்கவில்லை.கை கட்டி வாய் பொத்தி மாகாண சபையை ஏற்றுக் கொண்டனர்!அது வருமாறு:The Thimpu DeclarationThe Thimpu Talks - July/August 1985Joint statement made by the Tamil Delegation on the concluding day of Phase I of the Thimpu talks on the 13th of July 1985 It is our considered view that any meaningful solution to the Tamil national question must be based on the following four cardinal principles:The Thimbu Declaration1) Recognition of the Tamils of Ceylon as a nation2) Recognition of the existence of an identified homeland for the Tamils in Ceylon 3) Recognition of the right of self determination of the Tamil nation4) Recognition of the right to citizenship and the fundamental rights of all Tamils in CeylonDifferent countries have fashioned different systems of governments to ensure these principles. We have demanded and struggled for an independent Tamil state as the answer to this problem arising out of the denial of these basic rights of our people. The proposals put forward by the Sri Lankan government delegation as their solution to this problem is totally unacceptable. Therefore we have rejected them as stated by us in our statement of the 12th of July 1985. However, in view of our earnest desire for peace, we are prepared to give consideration to any set of proposals, in keeping with the above mentioned principles, that the Sri Lankan Government may place before us. இது இறைமையை அல்லாது ஈழ தேசிய சுயநிர்ணய உரிமையை கோருகின்றது என்பதைக் கண்டுபிடிக்க எதிரிகளுக்கு அதிக நேரம் எடுக்கவில்லை. அதுவும் அப்போது லெனினைப் படித்தறிந்த ஜே.ஆர்.ஜனாதிபதியாக இருந்தார். அவர் உடனடியாக ``இவர்கள் சுய நிர்ணய உரிமை பற்றிப் பேசுகின்றார்கள், சுய நிர்ணய உரிமை என்பது பிரிவினை, பிரிவினை தவிர வேறெதுவும் இல்லை.`` என உறுதிபடக் கூறி மறுத்துவிட்டார்.இம்மாண்டி தேசங்களை கட்டாயமாக இணைத்து வைத்திருக்கும் மகா பாரதத்தைச் சொல்லவா வேண்டும். குறைந்தபட்ச கோரிக்கையின் அடிப்படையில் இலங்கை அரசுடன் பேசத் தயாராகும்படியான உத்தரவுடன் திம்புப் பேச்சுவார்த்தை இனிதே நிறைவேறியது.இதைப் பகிரங்கமாகச் செய்வதற்கு யாரும் துணியவில்லை.தமிழீழ விடுதலைப் புலிகளைத் தவிர திம்புவில் கலந்து கொண்ட அனைவரும், திம்புக் கோரிக்கையைக் கைவிட்டு, இந்தியாவோடு கைகோர்த்து `புலி வேட்டையில்` இறங்கினர். இந்தச் சண்டாள சக உதிரங்களோடு போராட புலிகள் நிர்ப்பந்திக்கப்பட்டனர். இவ்வாறுதான் ``சகோதரப் படுகொலைகள்`` நடந்தேறின. கூடவே புலிகளின் பங்குக்கு `கந்தன் கருணை` போன்ற கோரங்களும் நிகழ்ந்தன.திம்புவில் இருந்த ஒற்றுமையைச் சிதைக்கும் இந்தியச் சதி நிறைவேறியது.இன்று வரை இந்த இந்தியத் துரோகம் பகிரங்கப்படுத்தப்பட்டு அம்பலமாக்கப்படவில்லை.சுய நிர்ணய உரிமையை பேரப் பொருளாக்கும் அரசியல் சந்தர்ப்பவாதம் 1985 இல் மீண்டும் புரட்சிக்கு பெருந்தீங்கிழைத்தது. இந்திய இலங்கை ஒப்பந்தம்:July 29-1987Text: THE INDO-SRI LANKA ACCORDகுறைந்தபட்ச கோரிக்கையின் அடிப்படையில் இலங்கை அரசுடன் பேசத் தயாராகும் பணியில் சமஸ்டிக் கட்சி குறிப்பாக திருவாளர்.அப்பாப்பிள்ளை அமிர்தலிங்கம் முன்னின்று உழைத்தார். இதன் இறுதி விளைவாக இந்திய இலங்கை ஒப்பந்தம் உருவாகி இந்தியாவுக்கும் இலங்கைக்கும் இடையில் கைச்சாத்திடப்பட்டது. இந்திய ஆக்கிரமிப்பு இரணுவம் வட கிழக்கில் புலி வேட்டையில் இறங்கியது. எஞ்சியிருந்த தனது தோழர்களை முகாமுக்கு அருகில் தன் சிறகுக்குள் வைத்துக் கொண்டது. இந்தக் கைக் கூலி வீரர்களுக்கு தலைமைக் கூலியாக இருந்த சுரேஸ் பிரேமச்சந்திரனின் `மண்டையன் குழு` விற்கு யாழ் அசோகா ஹோட்டலில் காரியாலயம் என்கிற சிறைக் கூடமும் சித்திரவதை முகாமும் இருந்தது. இது இன்றைக்கும் தண்டிக்கப்படவேண்டிய தேசத் துரோகக் குற்றமாகும்.விடுதலைப் புலிகள் ஒப்பந்தத்தை ஏற்கவில்லை. இந்திய இராணுவத்தை எதிர்த்துப் போராடி விரட்டி அடித்து வரலாறு படைத்தனர்.எனினும் `` எம்முடன் கலந்தாலோசிக்காமல் செய்து கொள்ளப்பட்ட ஒப்பந்தம் `` என்று சொன்னார்களே தவிர, ஈழ தேசத்தின் சுய நிர்ணய உரிமையை மீறி இலங்கையோடு இந்தியா தன்னிச்சையாக செய்து கொண்ட ஒப்பந்தம் என்று புலிகள் பகிரங்கமாக அறிவிக்கவில்லை.தியாகி திலீபனின் உண்ணாவிரதக் கோரிக்கையிலும் சுய நிர்ணய உரிமை உள்ளடக்கப்பட்டிருக்கவில்லை. இந்திய இராணுவத்தையும், அதன் கைக்கூலி ஆயுதக் கும்பலையும், மாகாண சபை முதலமைச்சரையும் விரட்டியடித்ததோடு, புலிகள் பேரியக்கமாக உருவாகினர். வன்னியின் பெரும் பகுதி அவர்களது முழுக் கட்டுப்பாட்டில் வந்தது.இலங்கை அரசு இதை ``விடுவிக்கப்படாத பிரதேசம்`` என அறிவித்து அழைத்தது. இங்கு புலிகள் தனிக்காட்டு ராஜா ஆனார்கள்.இந்திய இராணுவம் விரட்டியடிக்கப்பட்டதும் புலிகள்-பிரேமதாசா பேச்சுவார்த்தை திரிகோணமலைத் துறைமுகத்துக்கு உரிமை கோரிய பிரச்சனையில் முறிவடைந்து மீண்டும் விடுதலை யுத்தம் வெடித்தது. பேச்சுவார்த்தையில் சுய நிர்ணய உரிமையோ, பிரிவினைக்கு மாற்றான ஒரு தீர்வுக்கு பொது வாக்கெடுப்போ கோரிக்கையாக இங்கும் முன் வைக்கப்படவில்லை.புலிகள் யுத்தத்தில் ஊன்றி நின்றனர். யுத்தம் முன்னேறியது.புலிகள் ஒரு நிரந்தர இராணுவம் ஆகினர்.புலிகளின் தளப் பிரதேசங்களில் அதிகார நிர்வாக முறைகள் ஏற்படுத்தப்பட்டு ஆட்சி செலுத்தப்பட்டுவந்தது. தொடர்ச்சியான போரில் இறுதியாக ஆனையிறவுப் பெரும் படைத்தளம் அடித்து நொருக்கப்பட்டு ``முன்னூறு ஆண்டுகால அடிமைத்தனத்துக்கு`` முற்றுப் புள்ளி வைக்கப்பட்டதாக பிரகடனம் செய்யப்பட்டது.யாழ்ப்பாணத்தை நோக்கி முன்னேறக் கூடாது என்றும், இலங்கை அரசுடன் பேச்சுவார்த்தைக்குச் செல்லுமாறு அமெரிக்கா நேரடியாக அன்ரன் பாலசிங்கம் மூலம் கிளிநொச்சிக்கு தகவல் அனுப்பியது.மீண்டும் இந்தியப் படை தயாராக இருந்தது.புலிகள் பேச்சுவார்த்தைக்கு உடன்பட நிர்ப்பந்திக்கப்பட்டனர். 2002 இல் பேச்சுவார்த்தை ஆரம்பமானது.புலிகள் உள் அகத்தில் நேசித்து வெளியே சொல்லாமல் மறைத்து வைத்திருந்த சந்தர்ப்பவாத சுய நிர்ணய உரிமை, அக சுய நிர்ணய உரிமையாக வெளிவந்தது. சுய நிர்ணய உரிமையை தேசத்தின் குரல் அகம், புறம் என்று இரண்டாகப் பிரித்தது. இந்த அக சுய நிர்ணய உரிமை என்பது சேர்ந்து வாழ்வதெற்கென்றும், புற சுய நிர்ணய உரிமை என்பது பிரிந்து வாழ்வதற்கானது என்றும் விடுதலைப் புலிகள் அமைப்பின் அதிகாரபூர்வ தத்துவார்த்த தலைவர் கலாநிதி அன்ரன் பாலசிங்கம் விளக்கம் அளித்தார்.``துரோகி`` கருணா இந்த அ.பா.வை தலை சிறந்த ராஜதந்திரி என்று கூறியதில் உண்மை இருக்கத்தான் செய்கின்றது! சேர்ந்து வாழ்வதற்கு விவாகரத்து உரிமை கோரும் தம்பதிகளை உலகில் எங்கேனும் நீங்கள் கண்டதுண்டா மக்காள்!பேச்சுவார்த்தையில் ஈழமக்களின் அனுமதியின்றி, தமிழீழத்தைக் கைவிட்ட அதிகாரப் பகிர்வுத் திட்டமான, Internal Self Governing Authority (ISGA), தமிழில் கொச்சையாக `இடைக்கால அதிகார சபை` என்றழைக்கப்பட்ட நிர்வாக அலகு பரிசீலிக்கப்பட்டது. இது மிக அதிக அதிகாரங்களைக் கோரியிருந்தது. சொல்லப் போனால் இந்தியாவின் (தமிழக) மாநிலத்துக்கு உள்ளதைக்காட்டிலும் அதிக அதிகாரங்கள் உடையதாக-காகிதத்தில்- இருந்தது. சமஸ்டிக் கட்சிக்கு புலிகளால் கொலை செய்யப்பட்ட நீலன் திருச்செல்வம் மாவட்ட அபிவிருத்தி சபை முறையை சட்ட ரீதியாக வரையறை செய்தது போல, புலிகளுக்கும் புலம்பெயர் தேசங்கள் உள்ளிட்ட சட்ட வல்லுன சபாபதிகள் இதை வரைந்து தள்ளினர்.அதிகாரத்தின் அளவு எவ்வளவாக இருந்தாலும், தேசிய ஒடுக்குமுறைக்கு அதிகாரப் பகிர்வு என்பது ஒரு சீர் திருத்த முறையாகும். அதிக அதிகாரங்களைப் பெற்றுவிடுவதாலேயே ஒடுக்கப்படும் ஒரு தேசம் ஒடுக்கும் தேசத்துடன் சமநிலை பெற்றுவிட முடியாது.மேலும் சுய நிர்ணய உரிமை இல்லையென்றால் 30 ஆண்டுகாலம் இரத்தம் சிந்தி போராடிப் பெற்ற அதிகாரங்கள் பிறிதொரு சூழ் நிலையில் பறிக்கப்படுகின்றபோது அதை தடுப்பதற்கு உத்தரவாதம் இருக்காது. இந்திய இலங்கை ஒப்பந்தம்-13வது திருத்தம், இணைத்த வடக்கு கிழக்கு மாகாணங்களை JVP ஒரு வழக்கு வைத்து மீண்டும் பிரித்துவிடவில்லையா?!விடுதலைப் புலிகள் இராணுவ அமைப்பாக மட்டுமல்ல, அரசியல் அமைப்பாகவும் இல்லாத இன்றைய சூழ் நிலையில் அதை மீண்டும் இணைக்க முடியுமா? அப்போதே தற்காலிகமாக இணைத்து நாடளாவிய வாக்கெடுப்புக் கோரிய இந்தியா இப்போது உதவுமா?2002 பேச்சுவார்த்தையில் சுய நிர்ணய உரிமையைப் பேரப் பொருளாக்கிய சந்தர்ப்பவாதம் ஆனந்தபுர படுகொலையில் முடிந்தது.அரசியலில் சந்தர்ப்பவாதம் என்பது தற்கொலை தவிர வேறெதுவும் இல்லை.சுய நிர்ணய உரிமையின் நோக்கு நிலையில் ஈழப் புரட்சியின் இதுவரைகால வரலாறு என்பது,சுய நிர்ணய உரிமையைப் பேரப் பொருளாக்கிய அரசியல் சந்தர்ப்பவாதத்தின் வரலாறே ஆகும். ஆயுதப் போராட்டத்தின் துரித எழுச்சிக்கும், அதல பாதாள வீழ்ச்சிக்கும் இதுவே காரணம்.1983 ஜூலைப் படுகொலையின் 43ஆம் ஆண்டு நினைவாக நாம் அறை கூவுவதாவது:சுயநிர்ணய உரிமையைப் பேரப் பொருளாக்கும் சமரசவாத,சந்தர்ப்பவாத, சரணாகதிப் போக்குக்கு முற்றுப் புள்ளி இடுவோம்.நடைமுறையில் இதன் பொருள் இலங்கை அரசியல் அமைப்பின் ஆறாவது திருத்தத்தை நீக்கப் போராடுவதே ஆகும்.புரட்சிப் பாதையில் புதிய ஈழ விடுதலையை வென்றெடுப்போம்!புரட்சிகரத் தலைமையைக் கட்டியெழுப்புவோம்!!பின்வரும் முழக்கங்களுக்காகப் போராட ஒன்று சேருவோம்.அனுரா ஆட்சியே அந்நிய ஆபத்திலிருந்து நாட்டைக் காக்க, இலங்கை மக்கள் அனைவரையும் ஒன்றுபடுத்த அரசியல் யாப்பின் ஆறாவது திருத்தத்தை நீக்கு!ஏகாதிபத்திய அமெரிக்காவே, விரிவாதிக்க இந்தியாவே திரிகோணமலையில் கை வையாதே!அடுத்த ஆட்சிக் கவிழ்ப்புக்குத் திட்டமிடாதே!1) மூன்றாம் ஏகாதிபத்திய பொது நெருக்கடிக்கு உலக யுத்த மறு பங்கீடு மூலம் தீர்வுகாண முயலும் போர் தயாரிப்புகளை முறியடிப்போம்!2) நேற்றோ படை விரிவாக்கம், ஐரோப்பிய படை உருவாக்கம், இராணுவச் செலவின அதிகரிப்பு மற்றும் படைப்பெருக்கம் ஆகியவற்றை எதிர்ப்போம்!உலகெங்கும் வியாபித்துள்ள அமெரிக்கப் படைத்தளங்களைக் கலைக்கப் போராடுவோம்!3) உலகளாவிய ஏகாதிபத்திய,பாசிச எதிர்ப்பியக்கத்துடன் ஒன்றிணைவோம்!4) ஏகாதிபத்திய ஏஜெண்டுகளான பிராந்திய விரிவாதிக்க அரசுகள், உலகப் போருக்கு தம் நாட்டு உழைக்கும் மக்களையும்,அண்டை அயல் நாடுகளையும் தயார்செய்து, யுத்தத்துக்குள் தள்ளுவதை முறியடிப்போம்! 5) இணைக்கப்படாத இந்திய மாநிலமாக இலங்கையை ஆக்கும் இந்திய விரிவாதிக்கத்தை தோற்கடிப்போம்!ஆட்சிக் கவிழ்ப்புத் திட்டங்களை அம்பலப்படுத்துவோம்!6) தேர்தற் பாதையை நிராகரிப்போம், புரட்சிப் பாதையில் அணிதிரள்வோம்!7) ஆறாவது திருத்தம், பயங்கரவாதச் சட்டம், மற்றும் பாசிசக் கறுப்புச் சட்டங்களை நிராகரிப்போம்! 8) ஈழப்பிரிவினைப் பொதுவாக்கெடுப்புக்குப் போராடுவோம்!9) ஒடுக்கும் சிங்கள தேசத்தின், தேசிய ஜனநாயகப் போராட்டங்களோடு ஒன்றுபடுவோம்! 10) Trump இன் சிலுவைப் பாசிசம், நெத்தனியாகுவின் சியோனிசப் பாசிசம் ஒழிக!11) தேசபக்த ஈரான் போர் வெல்க! மேற்கு ஆசியாவில் அமெரிக்கத் தளங்கள் தகர்க!12) பாசிச இஸ்ரேல் அரசு ஒழிக! ஜனநாயக ஓரரசுப் பாலஸ்தீனம் எழுக!இறுதி வெற்றி ஈழமக்களுக்கே.புதிய ஈழப் புரட்சியாளர். 21-07-2026